")

Your Guide To Protecting Your Loved Ones

Planning for the future is an important step in making sure your loved ones are cared for, and a key part of this is properly setting up your Life and Accidental Death & Dismemberment (AD&D) insurance coverage. Whether you’re choosing beneficiaries for the first time or updating them after a life event, keeping your CUPE EWBT coverage up to date helps avoid issues and ensures everything runs smoothly. This guide provides practical steps for selecting the right beneficiaries, keeping your information current, and understanding the rules of your benefits plan, so you can make informed decisions that protect your family and reflect your wishes.

What Is a Beneficiary and Why Does It Matter?

A beneficiary is a person, a few people, or an entity that you name to receive the payout from your life or AD&D insurance policy if something happens to you. It’s important to choose carefully because this ensures your benefits go where you want them to.

Here’s why it matters:

- Your wishes are followed. The money will go to the people you choose, avoiding confusion or disputes.

- Faster payments. Without a clear beneficiary, the money may go through legal processes that can take a long time.

- Support for your loved ones. These benefits can provide financial help when it’s needed most.

Types of Beneficiaries

Primary Beneficiaries

Your primary beneficiary is the first person (or people) who will receive the coverage payout if you pass away. This designation is critical because it determines how your benefits will first be distributed. For example, if you name your spouse as the primary beneficiary, they will receive the benefits directly, ensuring financial support during a difficult time.

Without a primary beneficiary, your benefits may have to go through probate, which can delay payments and add unnecessary costs. If no primary beneficiary is named, the distribution of benefits may follow legal processes that might not align with your wishes.

Contingent Beneficiaries

A contingent beneficiary serves as your backup plan. They receive the benefits if your primary beneficiary is unable to, such as in cases where the primary beneficiary has also passed away. For instance, if your spouse is your primary beneficiary, you might choose your child or a trusted relative as the contingent beneficiary.

Choosing Your Beneficiaries

When selecting a beneficiary, consider:

- Relationship: Spouses, children, or other close family members are common choices.

- Responsibility: Make sure the person you choose can handle the benefits wisely and manage any associated responsibilities. If your beneficiary is a minor, you will need to choose a trustee who will be responsible for managing the benefit. You may also be able to assign a trustee for an adult beneficiary if you believe they may not be able to handle the responsibility. Once you’ve chosen your beneficiaries, make sure your beneficiaries understand their roles and responsibilities.

- Long-Term Needs: Consider how your choices will affect your family’s stability (financial or relational).

- Getting Professional Advice: A financial advisor or legal expert can help you navigate complex decisions and ensure your designations align with your overall wishes.

Considerations for Multiple Beneficiaries

You can name more than one beneficiary, each receiving a percentage of the benefit. When naming multiple beneficiaries, you can divide your benefits equally among beneficiaries or you can assign specific percentages to each. For example, you might leave 60% to one person and 40% to another, depending on their financial needs.

Document your choices on the beneficiary forms clearly and carefully. A common mistake with choosing multiple beneficiaries is not ensuring that the percentages add to 100%.

Consider Financial and Tax Implications for Beneficiaries

In most cases, the money paid out to Canadian beneficiaries from a life insurance policy is not taxable. This means the whole amount of the benefit can help your beneficiaries adjust and cope after your death.

However, you should look at your overall financial picture and consider the financial standing of your beneficiaries. Strategic planning can help maximize your benefits while minimizing any tax implications. Consider:

- Trust Arrangements: Trusts provide control over how benefits are distributed, making them ideal for managing larger coverage amounts or supporting younger or dependent beneficiaries. Trusts can also help ensure tax efficiency.

- Charitable Considerations: Naming a charitable organization as a beneficiary can align with your values while providing potential tax credits for your estate.

Financial and tax rules can be complex, especially for minor beneficiaries or beneficiaries in multiple countries. Checking with financial or tax advisors ensures your plan remains aligned with current regulations and maximizes benefits for your loved ones.

How to Designate a Beneficiary

Once you’ve chosen your beneficiaries, you will need to submit the required information to OTIP. You’ll need to complete beneficiary designation forms, that will require information such as:

- Complete legal names

- Relationship details

- Address

It’s important to pay careful attention when completing the beneficiary designation forms, otherwise the benefit payout may be held up or contested. Consider these steps:

- Review policy numbers and your details

- Ensure proper ordering and allocation of primary and contingent beneficiaries

- Submit clear, accurate information

- Submit information in a timely manner

Keeping Your Beneficiary Information Updated

When to Update Your Beneficiaries

Your life changes, and so should your beneficiary designations. Life changes, such as divorce or separation, can significantly affect your beneficiary choices. Update your beneficiaries promptly to ensure your beneficiary designations are revised to reflect your current wishes. For example, failing to update your designations after a divorce could mean benefits go to a former spouse instead of your intended recipient. Regular reviews—at least once a year—keep your information accurate and help prevent these issues.

Here’s when you should update your choices:

- After getting married or divorced

- If you have a child or adopt

- If your primary beneficiary passes away

- If your relationships or priorities change

A legal or financial advisor can guide you through updates and ensure alignment with any legal obligations.

How to Update Your Beneficiaries

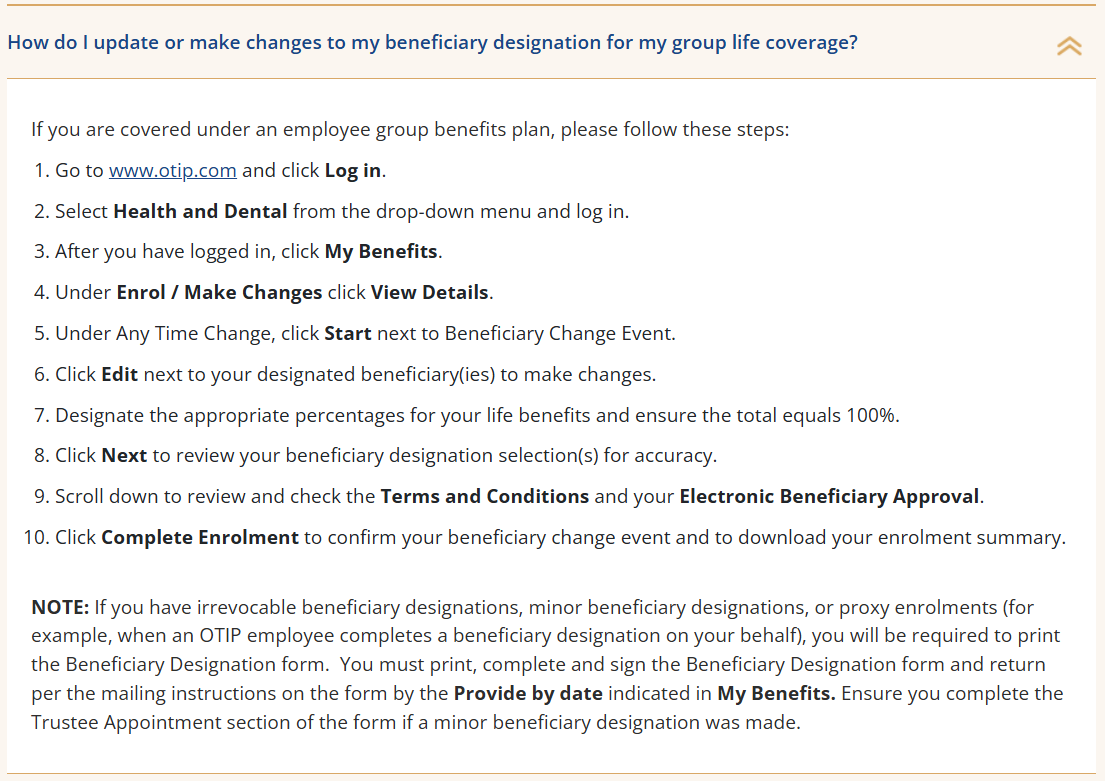

You can update your forms through your OTIP account or by contacting OTIP’s member services team. For more information, check out our Beneficiary Updates page.

Summary

Reviewing and updating your Life and AD&D insurance beneficiary designations is an essential part of protecting your loved ones and ensuring your wishes are honored. By taking the time to regularly assess your designations, you can avoid potential issues and ensure a seamless distribution of benefits when the time comes.

To get started, confirm that your primary beneficiaries are correctly listed. Add contingent beneficiaries as a backup plan. Revisit your choices annually and after major life events like marriages, births, or divorces.

Log into your OTIP account today to review your beneficiary details. Not sure how? Learn more here.